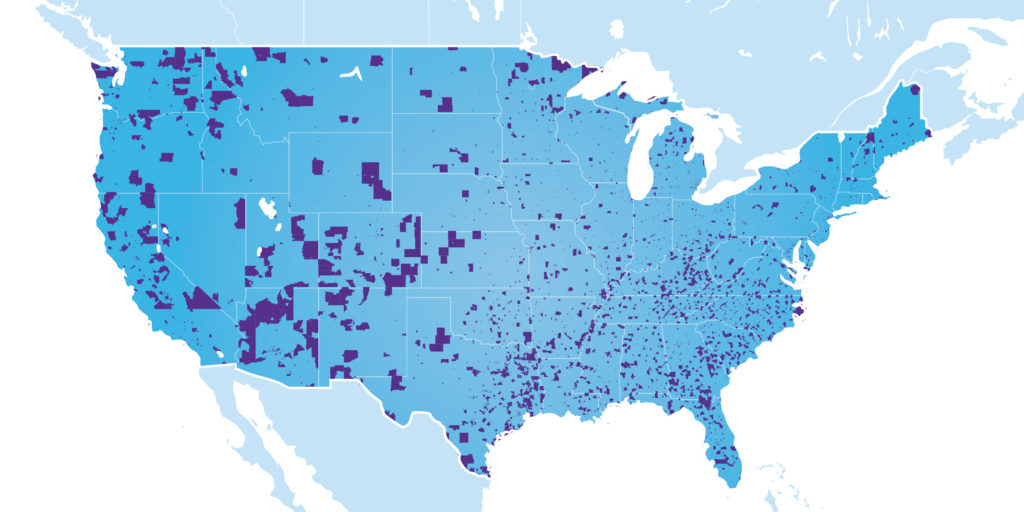

The Opportunity Zones program, established via the Tax Cuts and Jobs Act, aims to spur long-term private sector investments in low-income communities nationwide. Investors in Qualified Opportunity Funds participating within designated Qualified Opportunity Zones can take advantage of federal tax benefits in exchange for their contributions to economic growth and investment in distressed communities. Project sponsors can also benefit from lower-cost capital generated by the program. How it works: The Opportunity Zones program offers federal tax incentives for investing unrecognized capital gains in Qualified Opportunity Funds, which are investment vehicles created specifically for these purposes. The amount of benefit ultimately recognized depends on the holding period of the investment.

How to establish a certified Qualified Opportunity FundEligible taxpayers may self-certify to become a Qualified Opportunity Fund by attaching to its tax return Form 8996. No approval or action by the IRS is required. Where are the Opportunity Zones?Use the interactive map provided by Baker Tilly to search the complete list of Opportunity Zones that have been nominated, certified and designated. What’s next? There are a number of open issues surrounding the Opportunity Zones that require guidance from the U.S. Treasury Department or Internal Revenue Service. The first round of guidance arrived in late October and more is anticipated by year-end. We expect the additional guidance to focus on open questions related to operational issues, such as the availability of the 31-month runway for the deployment of funds in a direct investment model and the ability for residential rental property with a triple net lease to qualify as an active trade or business for the purpose of qualification as qualified Opportunity Zone business property. We will provide regular updates as the program continues to take shape and investment criteria and timing is outlined.

0 Comments

From Baker Tilly; The IRS recently issued Notice 2018-92, providing interim guidance on various requirements and procedures for 2019 federal income tax withholding. This alert focuses on the following items addressed by the Notice:

2019 Form W-4 will be similar to the 2018 form. In June 2018, the IRS released a draft of the 2019 Form W-4 and accompanying instructions, which included significant changes from the 2018 Form. In response to the resulting feedback, the IRS announced the redesign would be delayed until 2020. The Notice indicates the IRS will re-release the 2019 Form with minimal changes by the end of 2018. Employee requirements for submitting Form W-4If an employee experiences a “change in status” that reduces the number of withholding allowances they are entitled to claim (for additional details regarding these allowances, please see our earlier alert), they generally must submit an updated Form W-4 to their employer within 10 days of the change. In January 2018, the IRS announced that employees whose allowances were affected solely by changes wrought by the Tax Cuts and Jobs Act (TCJA or the Act) were not required to submit updated Forms in 2018. The Notice extends this grace period through April 30, 2019. Accordingly, any such employee should submit an updated Form by May 10, 2019. Under prior law, employees who failed to furnish a Form to their employer were treated as single with zero exemptions for determining their withholding requirements. Ultimately, the IRS and Treasury Department intend to withdraw and modify existing regulations, and issue guidance to allow employees to be treated as single, but entitled to certain additional allowances. However, in the interim, employees who fail to furnish a Form will continue to be treated as single with zero allowances. Section 199A deduction For taxpayers that may be entitled to a deduction under section 199A (qualified business income deduction), the Notice allows such taxpayers to use an estimate of their anticipated 20 percent deduction to determine their withholding allowances to report on the Form W-4. As a reminder, wages are not qualifying income for purposes of the section 199A deduction. Alternative withholding methods As an alternative to using the personal allowances worksheet included with the Form to arrive at the number of allowances to claim, the Notice allows taxpayers to use the withholding calculator released by the IRS in early 2018. The Notice cautions this approach should not be used by taxpayers in certain tax situations, including but not limited to being liable for alternative minimum or self-employment taxes, or having long-term capital gains, qualified dividends or taxable Social Security benefits. We strongly advise that, if used, the calculator results be independently verified, particularly with the assistance of the employee’s tax advisor. The IRS and Treasury intend to discontinue the combined income tax and employee FICA tax withholding tables for use in completing the Form due to the “unintended complexity and burden of the method.” Withholding from pension, annuity and other certain deferred income: Generally, payors of certain pensions, annuities and other certain items of deferred income are required to withhold from such payments pursuant to the number of allowances the recipient claims on their Form W-4P, Withholding Certificate for Pension or Annuity Payments. The Notice provides that similar to previous years, a recipient who has not submitted Form W-4P will continue to be treated as married and entitled to three withholding allowances, as applied to the 2019 withholding tables. |

AuthorArchives

March 2020

CategoriesThe NY Accounting, Tax and Advisory Expert Blog |

RSS Feed

RSS Feed